Клуб мировой политической экономики |

» | Публикации |

How Bad, How Long? The current financial crisis impact on the real sector | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Клуб мировой политической экономики предлагает вашему вниманию доклад на английском языке Директора Высшей школы исследований по социальным наукам CEMI-EHESS (Париж) профессора Ж.Сапира, в котором дается анализ основных причин нынешнего переполоха в сфере международных финансов, начавшегося с кризиса на рынках недвижимости и ипотечного кредитования в США и Великобритании (т. наз. Subprime-кризиса), и его влияния на реальный сектор экономики. Центральный тезис доклада сводится к тому, что кризис в реальном секторе будет намного более глубоким, нежели это кажется сегодня большинству аналитиков. Этот кризис, как считает проф. Сапир, будет последовательно нарастать в период осени 2008 — зимы 2009 гг. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

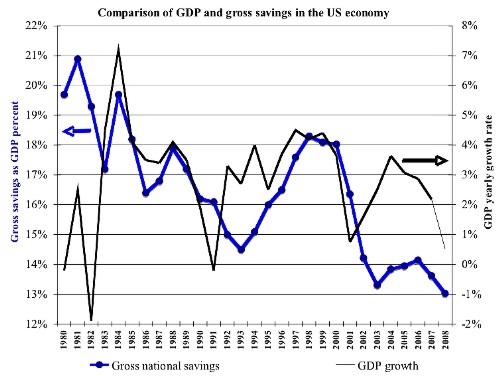

The present paper focuses on the possible extent of the current crisis as induced by the global financial turmoil the so-called “Subprime” crash induced. It is to focus on impacts on the ‘real’ economic sector[1]. The main thesis of this paper is that the ‘real’ sector crisis is to be probably much deeper than what most analysts believe right now, but is to unfold only progressively during Fall 2008 and Winter 2008-2009. A very dangerous feeling of confidence has been fuelled during late April and May 2008 because current economic data (which at best cover only 2008 first quarter) are less bad than expected[2]. Actually, most medium to long-term trends in the US economy but also for various Western European countries are showing that fundamentals of the ‘real’ sector are not good. The financial crisis has not been a pure speculation developing independently from the rest of the economy. The financial sector ran into troubles because there was something badly rotten in the real sector. Finance has been used as a temporary and provisional fix-up for structural troubles nobody had the political will to address. To some extent too, this lack of will, as well as the current unwarranted feeling of confidence translates the present situation in economics, where liberal ideology has deeply undermined scientific approaches. The “Theoretical Dimension” of the current crisis could well prove to be as important as the financial dimension. The present paper structure is to reflect issues here above mentioned. It will begin by a section devoted to a review of assumptions and theoretical issues underlying the current crisis understanding. A second section will address the issue of actual recessionary forces in the US economy. The exact nature of growth during 2000-2007 is to be addressed and to what extent it was a sustainable path questioned. Understanding ‘real’ roots of the financial crisis allows for a better forecast of how bad the recession is to be in the US economy. It shows that a “back to the normal” scenario is not possible and that the growth model of the late 90’s is to be seriously amended to allow for a balanced and sustainable growth path. The third section is to address dynamics in various key European economies. Western European countries are to be discussed first as they actually display a quite diverse picture. Despite the EU and even the Euro Zone, Western European economies are not showing common macroeconomic and structural dynamics. The economic asymmetry between France and Germany could even strain the Euro zone up to the collapse point. Eastern European economies are to be discussed after, as growth here is highly dependent from activity in Western Europe. If major Western European economies are to slow down to a considerable extent, the impact on Eastern Europe is to be significant and trade and budget imbalances could become a serious issue by 2009/2010. Long-term growth in Eastern European economies would imply a better acknowledgement of the growth potential the Russian economy is currently presenting. 1. Assumptions and Theoretical IssuesSo far implications on the ‘real’ economic sector have not been fully understood. This explains why published forecasts on the recession or possibly depression in the US economy but European economies as well have been so diverging during 2008 first quarter[3]. The central assumption of the analysis presented here is that the “Subprime” crash has been a trigger but not the main cause of the present crisis. I.1. Assumptions and conflicting explanations. Economic disorders are going much farther and deeper than what developed on the US (but also British…) mortgage market. If, from a day-to-day perspective, unregulated global finance looks as the main culprit, there are good reasons to think that the liberal institutional dismantling, which led to the financial side of the crisis, has actually been a symptom of a more global disorder. This assumption, if vindicated, could entail a pivotal re-assessment of the current crisis. Two explanation main lines of the so-called “Subprime” crisis are possible. They are openly conflicting and would have deeply opposed consequences. The first one, which so far is predominant, sees the current crisis as the result of limited policy mistakes in the financial regulation field. Regulatory agencies, and to some extent rating agencies too, are then to burden the blame and solutions could be relatively easily implemented. In this scenario we could emerge from the current crisis relatively quickly (by late 2009) and in an economy mostly unchanged, be it at national or international level, but for a revamping of financial regulations. An extreme form of this position is the one defended by some authors, like Alan Greenspan the former FED president, who has presented financial bubbles as an inevitable part of a capitalist economy[4]. It is however to be reminded that financial bubbles have been nearly non-existent in Western economies from 1945 to 1985. Even the famed business cycle seemed to have disappeared[5]. This openly contradicts the view of an inevitability of large-scale financial disorders. In the same time, a comparison of business cycles in Western economies as described by W.C. Mitchell on the basis of pre-1939 data[6] has shown that both the size and scope of economic fluctuations are directly related to the nature of the growth model. It is then interesting from Sociology of organization point of view, but extremely disquieting from an economic policy point of view to see to such extent some major former of present players in the Central Banking game have lost the “historical memory” of the XX Century capitalist economy. It is either a problem of incompetence or a testimony to the fact that ideology is dominating scientific analysis in today economics. There is however a second possible explanation line. Finance has been de-regulated because of pressures building up in the ‘real’ sector. Finance had to accommodate to a much deeper disorder resulting from economic and institutional reshaping induced by “Conservative Revolutions” implemented from the 80’s[7]. This is particularly obvious in the US economy, but could be applied to other countries too. Household credits became central to the neo-liberal growth model because inequality have undermined and to some extent destroyed the real growth engine of the 1950’s to the 1980’s, that is the “middle-class”[8]. If so the current crisis is to be understood as neither a “natural” phenomenon nor the end of just a given business cycle but as a key moment a global political economy cycle: the crisis of neo-liberal economics. If this assumption is to be validated then the current crisis extent and duration are to be much more severe than what is implied by the first line of explanation. We would not exit from the crisis without much widespread institutional and policy changes than ones involved by the first line of explanation, and going much farther than just an attempt in re-regulating finance, even if such a re-regulation is clearly badly needed. A side effect of the second explanation line would be that the current crisis is not to be “global” in the common sense but to hit disproportionately countries whose economic institutions have been more fully reshaped by “Conservative Revolutions” than others. This could explain a growing heterogeneity among OECD economies, and particularly among European Union economies. This side effect has also another important implication. The current “decoupling” of Asian but also Russian economies with trends predominating in the US and European economies is here to be noteworthy. Behind what looks like another financial crisis in a string of crashes beginning in the 1987 stock-market slump we could well be confronted to an important economic power shift. I.2. Theoretical issues. As in every large-scale crisis, several theoretical points have come to the limelight. The huge support the FED gave to private banks raised obviously the issue of a moral hazard situation. This is quite systematic in any financial crash when Central Banks have to play their lenders of last resort act. However, other important theoretical issues have been at stake. The lack of prudential restraint in lending has been noteworthy during the US Mortgage-market bubble, to the point some observers have even spoken about “aggressive lending”[9]. We contend that this lack of prudential restraint has not just been the result of technical mistakes or even a lack of awareness to possible consequences of financial innovations. This is not to say that there have been no technical mistakes. Actually Basel-II accounting rules have played significant a role in worsening the financial crisis impact[10]. There are few doubts too that rating agency have been lenient or at the very least ill-adapted when facing the development of structured finance portfolios. This is pretty well known, but can’t explain how the crisis developed and why it became so global. If technical regulations are certainly to be revamped, to believe that the re-assessment process the current crisis is to induce would stop there and then would be deep a mistake. The financial deregulation process[11], which culminated in the Glass-Steagall Act demise of 1999[12], is also to be questioned. Financial regulations introduced in the wake of the 1929 Crash, and including the Emergency Banking Act of March 9th, 1933[13], were designed to restrict competition and avoid savings to be freely mobilized by financial institutions for speculation. The main idea behind these regulations was that financial markets were unstable and banker expectations too much prone to go wild under pressure of pair’s competition. The 1933 regulation package was progressively dismantled from 1980 on. The first move was the Depository Institutions Deregulation and Monetary Control Act of 1980. This process culminated with the Gramm-Leach-Bliley Act of 1999, which ultimately destroyed what had been left of the Glass-Steagall Act and allowed deposit and investment banks to merge[14]. It is known that the Gramm-Leach-Bliley Act resulted from a strong and persistent lobbying from the largest US bank, Citicorp (now known as Citigroup), whose arguments found friendly listening among President Clinton’s administration, and particularly the former Secretary of the Treasury, Robert Rubin. Once President Clinton signed the act into a law on November 12th, 1999, Citicorp hired Robert Rubin as a member of its office of the chairman. The Gramm-Leach-Bliley Act allowed consolidation of merging between banks, insurance companies and investment banks, which had begun in 1993-4 and would ultimately have been found illegal once the temporary waiver process suspending some of the Glass-Steagall Act aspects would have ended[15]. There is no doubt that the deregulation policy created a lenient environment, which helped speculation to reach new summits. One has to remember that the Depository Institutions Deregulation and Monetary Control Act was followed by the strong speculation, which ended in 1990 in the tremendous “Saving and Loans crisis”, the late John Kenneth Galbraith called “the largest and costliest venture in public misfeasance, malfeasance and larceny of all time”[16]. The US government was forced to bail-out most of US savings banks in a move costing then 123.8 US Dollar billions on a total of more than 150 Billions, the balance being supported by the banking industry[17]. This crisis was a major event, inducing a severe recession in the US economy in 1990-1991[18]. But if the Depository Institutions Deregulation and Monetary Control Act can be put on the President R. Reagan strident liberal ideology, neither the “Saving and Loans” crisis nor the arrival of the Clinton’s administration actually changed the mood and the move toward a deeper liberalization of US finance. The demise of the Glass-Steagall Act has certainly been an important turning point, because it had been drawn historically with the aim of preventing deposit bank to enter a speculative game. The Gramm-Leach-Bliley Act certainly weakened financial regulations to a very dangerous extent and created a “context”, which definitely played an important role in the setting of the mortgage-market bubble. Paul Krugman pointed to Senator Phil Graham, currently one of J. Mac Cain’s economic advisers, constant advocacy of financial services deregulation as one of the main cause of the “Subprime” crisis[19]. Nevertheless, as fateful it could have been, this event could not explain all. Competition among mortgage brokers and more generally speaking among various kinds of financial actors (Banks, Insurance companies, Hedge-Funds) has been instrumental in what can be retrospectively seen as a typical case of dereliction of (prudential) duty. Inducing new households into mortgage loans became so important for mortgage brokers in what looked like an ever-expanding market that prudential behaviour was seen as an unbearable limit to market power[20]. This explains how and why mortgage-market special compartments, which were of limited importance in the 90’s became so relevant by 2005/2006. The same can be said about the blossoming of new and highly complex financial derivatives like CDO’s-squared. Their fast development was a direct result of the cut-throat competition among financial actors. Even the IMF, in its Global Financial Stability Report of April 2008, had to acknowledge that: “…some complex and multilayered products added little economic value to the financial system. Further, they likely exacerbated the depth and duration of the crisis…”[21]. Financial innovation does not happen in a vacuum and its path is to a large extent the result of competitive pressure. Individual economic agents don’t shift to an “irrational” kind of rationality because of the plain moon like characters in Werewolf novel. Competition, when the future is uncertain, fosters in a logic way this kind of “irrational” rationality. Markets turn into new gambling spaces not because there is not enough competition but because there is too much and stakes for every participant are too high. Far to promote efficiency, competition has actually seriously undermined financial stability and led to a string of unsustainable decisions. This is a classical case of adverse selection and raises the issue of how much competition is actually needed in finance. Microeconomics of adverse selection is known for quite long[22], but their macroeconomic impact seems to have been seriously understated. The actual value of competition policies, as promoted in the wake of “Conservative Revolutions” is to be seriously re-assessed. More generally speaking, the paradigm of competition is to be seriously questioned. It is a point Joseph Stiglitz raised in his 2001 Nobel Prize lecture[23], which needs to be forcefully rammed home to many economic policy decision-makers[24]. Highly competitive markets are not necessarily the best coordination tool we need and fostering more competition could be efficiency destructive because no market can be informationally efficient in the real-world economy[25]. Another point frequently raised in reports commissioned on the “Subprime” crisis is the impact of economic context on individual behaviours. The already quoted IMF report then states: “…the benign performance of credit markets since the early part of the decade gave investors a false sense of security”[26]. The same report insists on “normal market conditions” as a perquisite of accounting rules[27], and the Financial Accounting Standards 157 itself defines the “fair value” concept as a price a market defines in “orderly conditions”[28]. The IMF now acknowledges that such rules have created “flowed metrics for evaluating the default risk of portfolios”[29], and that the fair value is “compounding market instability”[30]. Albeit belated these acknowledgements are to be welcomed. However one can’t escape the feeling that the IMF, a well-known staunch defender of axiomatic approach in economics when it comes to inflation, has been pushed back to pure empirical “story-telling” as in some institutionalist works it earlier vilified. Actually both the impact of contextual environments on individuals’ behaviours and the presence of huge preferences instability under surprise events have been well known for nearly three decades[31]. The impact of “surprise” on market-based expectations has been thoroughly analysed even earlier[32]. The very fact that the traditional theory of rationality, on which mainstream economics are heavily lying, has no actual grounding is now a well-known fact[33]. Implications for economic theory as well as in specific markets have been thoroughly analysed[34], and an alternative view of rationality promoted[35]. The considerable increase of gambling activities in the USA during the late 80’s and 90’s suggests that a powerful “framing effect” had been generated by institutional changes the “Conservative Revolution” has generated[36]. It is interesting to note that the same link between gambling (legal and illegal) and speculation (on both real-estate and stock markets) can be found on the eve of the Big Depression[37]. One can then do clearly better than just “describe” the process leading to the “Subprime” crisis. This is not to say that an informed description is not necessary, or that “story-telling” is not part of a scientific methodology. However, what really matters is the fact we can now explain, from the micro-economic level up to macro-economic consequences how and why this story, in a way so similar to previous financial crisis stories, developed. The combination of “framing” and “endowment” effects, with the demonstrated informational instability of markets gives us tools needed to understand why finance is to go sick on a regular basis but for constraining regulations stringently limiting competition. The awful repetition of financial crisis from the mid-80’s up to the present one is creating a false impression that they are as inevitable as a strong thunderstorm after a couple of very hot days. However, this feeling is falsely grounded. We don’t have to forget the fact capitalist economies lived without financial crisis from 1945 to the mid-1980’s. If financial bubbles and crashes are not part of our life as an “inevitable evil” like bad weather, then there is an analytical imperative to understand how they are generated as well as a normative imperative to devise policies preventing them. What new advances in micro-economics bring us is the possibility to go beyond description and to have macro-level policies grounded on solid theoretical ground. This probably is not to be enough. Developing a new theoretical understanding of financial crisis is not be useful till we will stay inside the framework “Conservative Revolutions” of the 1980’s created. This implies that designing policies helping us to get through consequences of the current crisis at the lesser cost are not to come out from any theoretical heaven without a significant ideological and political conflict. I.3. Reversing monetarism and the Neo-liberal counter-revolution. The current financial crisis is then raising a two-pronged issue in the theoretical battlefield. First, it highlights that major financial institutions are, like the French military establishment in 1939, “a war behind”. They have not integrated into their own theoretical framework progresses made a generation ago. Assumptions about individual agent rationality, individual preference ordering and stability used in macro-economic model widely used by mainstream economists have been proved false. This is particularly damning when one knows that one of the leading authority on finance and real-estate markets, Robert J. Shiller is openly using results of recent researches on rationality and preferences[38]. Second, what is clearly needed now is a macroeconomic theory consistent with progresses made in microeconomics. Changes in microeconomics are not limited value niceties. They imply a return to the “money illusion” theory and a demise of the “rational expectations” theory. To the very contrary of the Lucas-Friedman credo, nominal rigidities matter[39]. Charles Kindleberger contended as early as 1978 that even if maximizing rationality could have a heuristic interest, rational expectations were a very dangerous assumption when one looked to financial crisis. He wrote: “The a priori assumptions of rational markets and consequently the impossibility of destabilizing speculation are difficult to sustain with any extensive reading of economic history”[40]. However, this position was unable to convince mainstream economists because in their axiomatic approach of economics they have no place for economic history[41], to the difference of economists committed to institutional economics. Hence Hyman Minsky was probably the one who better reacted to Kindleberger book[42]. Minsky wrote: “It is now clear that the power of the rational expectations/new classical macroeconomic revolution was derived from the heroic specification of the model that agents use to guide decisions, rather than upon the proposition that agents use “all” of the available information in making decisions where “all information” takes the form of models (theories) of how the world behaves”[43]. Minsky then went forward comparing how Keynes’s approach to uncertainty could be compared to Herbert Simon’s bounded rationality approach[44]. He concluded that if both Keynes and Simon were converging on the relevance of uncertainty to understand “real-world” economics, they went apart where the bounded rationality tradition still retained the view that preference systems were to some extent exogenous to the actual environment of the economic agent and where Keynes supports the view that nominal prices and values directly shape the economic agent behaviour in an interacting process with other agents[45]. It can be added here that advances in experimental economics or applies psychology, which produced the “framing effect” and the “endowment effect” are giving the scientific grounding to Keynes, Kindleberger and Minsky intuitions. We now have “proofs” in the classical scientific meaning that individual agents don’t have an ex-ante, independent rationality, but that the rationality of a given choice is “constructed” in a given context and through given inter-action processes with other agents, including of course wealth distribution and inequality. This implies, as stated by Minsky, that sharp changes in the behaviour of agents are possible, with a strong impact on economic dynamics. These theoretical progresses matter much beyond the sphere of micro-economic theory[46]. To a large extent, they give traditional Keynesian economics, like they have been defended by Hyman Minsky or Paul Davidson sound micro-economic groundings, to the contrary of mainstream economics, which are now looking as inconsistent in their link between micro and macro levels. They imply on the analytical side that we have to model an economy where rigidities are probably more pervasive than flexibility[47]. Assuming flexible markets is dangerous a mistake. On the normative side now, this implies that more competition can by harmful and that sometimes more rigidity could be needed. They imply that decentralized maximisation processes don’t generate necessarily and aggregated optimum. Macroeconomic models are to reflect the real-world economy and integrate those theoretical progresses or they would be useless. An important consequence is that the “Conservative Revolution” view on social security, one putting the emphasis on individual responsibility and financial market, is clearly adding to a considerable extent to macroeconomic instability. It is doing so in two different ways. First it has created a strong ideological bias in economics preventing an effective assessment of financial threats and possible crashes. Second, it generated a strong change in social structures characterized by increased inequality and a greater personal uncertainty for the large population majority. This change has fuelled both a powerful endowment effect and a framing effect, which have created a situation particularly prone to an unbound speculation. To some extent what is now acknowledged as “technical deficiencies” in the banking supervision system and in rating agencies could be linked to the psychological context changes generated by “Conservative Revolution” have created. Financial pathologies have not evolved separately from changes in the “real” sector. An unsound “real” economy can’t generate a sound financial sphere. As a fitting example, the world-wide development of the pension-fund system engineered by the dismantling of State-supported retirement benefits is now understood to have been major a mistake[48]. It is of interest to note that Robert J. Shiller, who is now acknowledged as an authority in finance in some ways, expresses the same doubt about the micro and macro value of pension funds than radical economists[49]. I. What extent for the US recession?Because the crisis originated from the US mortgage market, its impact on the US economy has been so far the most severe. In the same time, the mortgage market crash is shedding a new light on the last decade US growth pattern and more generally on the US economy till the mid-1980’s. II.1. The US “false growth” from 1999 to 2007. The US economy has been put forward during the last years as a tremendous success, worth duplicating in European countries. Actually the US economy has experienced an average 2.6% yearly growth rate from 2002 to 2007, which is the lower rate since the early 80’s. The average yearly growth for the 1983-1990 expansion period has been 4.0% and for the 1992-2000 expansion 3.7%. This has been to a large extent the result of a lackluster wage and salary income real growth, which didn’t exceed 1.8% a year in average compared to around 3.7% a year for 1993-2000, combined to a relatively slow increase in employment. By end 2007, when employment peaked in the US economy, the level was still under the 2003 figure. By any extent the years 2002-2007 expansion period has been the weakest of any expansion since the end of World War II. It is important to note here that productivity growth has been at a relatively low level during those years, at a time when inequality was growing fast[50]. What prevented growth to be even weaker was a spectacular drop of the gross saving rate, which mostly originated from a drop of household saving rates, achieving an historical low of 0.4% of net disposable income in 2007 against 2.4% in 2002. Enterprise savings only partially filled the gap hence created and the gross national savings as GDP percent fell from16.6% for the 1992-2000 expansion period down to 13.8% for 2002-2007. This period appears then to be quite unusual and at odds with characteristics of previous expansion episodes in the US economy. Movements of GDP growth and gross savings look quite related from 1982 to 2002, but the relative post-2002 expansion has not been followed by a significant rebuilding of the gross saving rate after the strong post-2001 fall (figure 1).

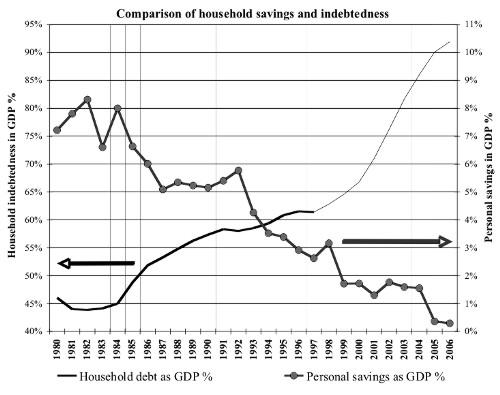

Unusual characteristics of the US recent expansion have already been noted in a previous paper[51]. What sustained too expansion has been the high level of home equity extraction rising real-estate prices allowed. Not only was the housing bubble creating a strong positive wealth effect but, through the mortgage market. Through cashing-out from their houses, US households obtained a yearly average of more than 51 USD billions a year between 2002 and 2007 (with a 80 USD billions pike in 2006) against a yearly average of 5.8 USD billions between 1993 and 2001. Home equity extraction, which amounted for 0.4% of Real Personal Consumption Expenditures between 1993 and 2001, jumped to 2.4% between 2002 and 2007[52]. This single fact implies that every things being equal the Real PCE got a yearly boost of 2% from home equity extraction between 2002 and 2007 by comparison of what it got during the 1993-2000 expansion period. Note here that this Real PCE 2% yearly growth attributed to the home equity extraction mechanism has balanced the real wage and income nearly stagnation we mentioned before and corresponds to the actual income growth rate obtained in the French economy. This allowed households to maintain high spending rates despite the above-mentioned lackluster wage and salary growth. Actually, if we add these 2.0% to the actual wage and salary growth experienced between 2002 and 2007, we are falling back to the 3.7% real wage growth rate of the 90’s. This however has implied a fast increase in household indebtedness, as the home equity extraction was obtained through mortgage roll-overs, reaching previously untold levels in the US economy (Figure 2).

It is then possible to speak of a “false growth” to describe the US economy during 2002-2007. Growth had been obtained through manipulation of mechanisms unsustainable in the mid-term. Pressure exerted on industrial wages through the globalization process explains why real wages and salary income have increased so little compared to previous expansions[53].

This pressure has been greater after 2002 than in the 90’s because low income-level countries have begun a technological ladder-climbing process, which has not been followed by a commensurate increase in local wages (table-1). It is now impossible to defend the idea that the WTO sponsored globalization has had a positive or neutral effect on developed countries macroeconomics. However, the globalization impact has been compounded with “Conservative Revolution” effects, including deregulation and curtailing of social benefits. The upward trend in household indebtedness clearly begins in the early 80’s. Economic policies, which are usually known as “Reaganomics”, have undermined the US middle-class, which actually has been the growth engine since 1945. The 90% lowest US incomes were amounting for 66.99% of the US total income in 1979 and only 54.34% in 2005. If the average income still increased the median income has been nearly stagnant since 1996[54]. Tax-break laws implemented from 1981 onwards have had a deep and pervading effect on income distribution, tremendously increasing inequality[55]. This trend has not been reversed under the Clinton’s administration. Actually, between 1990 and 1999 savings and debt increase were balanced, when in the 70’s and the 80’s, yearly savings were significantly higher than the yearly debt increase. “Conservative Revolution” policies have aimed at reducing the share of wages and salary incomes by comparison to corporate profits and have considerably reduced public spending, which had a high equalizing effect.

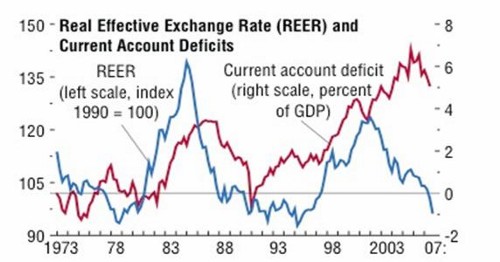

Combined to globalization effects, these policies have considerably depressed the Personal Consumption Expenditures potential. This would have reduced growth much earlier but for the switch to credit-backed consumption. However, with income growth constrained, lending progressively has out stripped repayment potential. Household savings fell accordingly in a spectacular way during the 90’s and the beginning of the XXI Century (Table 2). What made this evolution possible was the strong “framing effect” an upward “bubble” is generating. When the NASDAQ bubble collapsed in 2000, speculative expectations shifted to the real-estate sector. The rise in real-estate prices then induced a strong “endowment effect”, which progressively made borrowers deaf to any prudential advise. On the lender side, the cut-throat competition environment deregulation has created quickly an adverse selection process. Hence a globally unsustainable process set in from both sides. There is here no point to try fingering out “irrational” behaviours. If we admit that rationality is always “framed” or context-dependent and that preference reversals are the logical reaction to surprise, then the unsustainable growth of 2002-2007 has been the logical result of rationality. The point missed by mainstream economists is that market-generated “rational” behaviours are not necessarily consistent with mid to long-term stability and growth. Market rationality is consistent with the environment a given market is generating at a given time and no more. By early 2007 the US economy has crossed its stability threshold by a large extent but it was the “surprise” induced by initial bank and mortgage-brokers collapse, which generated a major change in perceptions. The development of the US mortgage bubble has then been a symptom of much deeper economic and social disorders. By the same token, the spectacular explosion of structured finance and the softening of prudential behaviours inside financial institutions has been the “rational” result of a global context, framing choice perception, creating new endowment perception and generating so strong a competitive pressure that a “do or die” mentality pervaded at every level[56]. This is an important point to understand how bad the recession is to be in the US economy. II.2. Is the US economy heading toward a deep and protracted recession? Three factors are pointing toward a severe and protracted recession. Their cumulative effects are to be felt at the very least till the end of 2009 and probably latter. First, the wealth effect is now to go downward, for several reasons. With brutal drop in house prices, the home equity extraction is to be considerably reduced. If it would go back to its 1993-2000 levels, this would imply a yearly reduction of the real PCE by at least 2% everything being equal. Note here that would stock prices go down during 2nd or 3rd 2008 quarter, the reduction could be greater. This reduction is to extend at very least till end 2009 and probably till summer 2010. In previous recession, the household saving rate acted as a kind of income buffer. Households reduced their savings to compensate for falling income from various sources. With a 0.4% rate it is clearly obvious that the saving rate is not to play its usual buffer role. As pension funds have been severely hit by the fall in stock prices till end summer 2007, US households are to be under a strong pressure to reconstitute both their wealth and savings. To the contrary of previous recessions, the saving rate is then to increase, becoming then pro-cyclical. Note here that a return to a 2.4% rate as in 2002 would imply a further PCE reduction of 2%. However, what has been described here is in a way a pure computational approach. What is still not known is to what extent the new context, with the looming threat of mortgage foreclosures and with many family in the neighbourhood expelled from their home, is to impact on US household preferences ranking. The dynamic side of preference reversals is to be acknowledged even if it is nearly impossible to give a precise forecast for such a process. One cannot exclude the possibility of households overreacting to the new context and increasing their saving rates to a much larger extent than what is usually forecasted. One result of empirical and econometrical studies done so far on the wealth effect is to show that: “…consumers react more strongly to negative shocks of the value of their liquid stock-market assets than they do to shocks to any other component of total wealth”[57]. One result of the home equity extraction mechanism is that real-estate has become a highly liquid wealth asset between 2002 and 2007. Then one can forecast a particularly strong downward consumer reaction when all consequences of the home-prices fall are to be acknowledged. The effect of the credit constraint now snowballing from the mortgage market to the credit-card and auto-credit markets is also difficult to predict as it could massively change household expectations. On both markets the share of delinquent credits has been increasing fast since December 2007. By early February 2008 it was announced that credit card companies were to write-off 5.4% of their prime card balances against 4.3% in January 2007[58]. More than 7.1% of loans related to personal vehicles and cars were in trouble against 6% by January 2007 and personal bankruptcy filings, which had significantly decreased after the 2005 Federal law making much harder for households to wipe out their debts, are again increasing significantly. Even if the US government is to implement a larger relieve plan than what Secretary Paulson has designed so far, one can reasonably assume that the wealth effect is to play a deep downward role on the US economic activity at least till 2010. Second, if bad news are coming from the wealth effect, the situation in the wage and salary income field is no better. As unemployment has again been on the rise since 2008 first quarter downward pressures on real wages are to be quite strong. As the total number of wage-earners is now diminishing, the global wages and salary income inflow is at best to stagnate. It could not compensate for the downward wealth effect. At the very best the real wage and salary income growth could be at 0.5% for 2008 and 2009. Combined to the wealth effect, this could imply a reduction of real Personal Consumption Expenditures by 1.5% to 3.5% a year in the 24 months going from summer 2008 to summer 2010. To what extent the fall of internal consumption could be compensated by investments and exports is difficult to assess. US investments have been quite low for a while and there would be some good reasons to expect an increase in forthcoming years. However in a recession the private sector is not very eager to increase its investment effort. Usually a public investment policy would be an effective contra-cyclical tool. However, as it is to be explained latter, the US budget is to be severely constrained for 2009 and 2010 fiscal years. A low US Dollar change rate could boost US producer competitiveness. Nevertheless, if US exports increased during fall 2007 and early winter, the process has been much smaller than expected. If the US Dollar real Effective Exchange Rate has went down to a considerable extent, the current account deficit is still very high (Figure 3). It is also true that so far the US Dollar Real exchange rate has fallen more compared to the Euro than to East-Asian currencies. Shifting most of the US export potential toward the Euro-Zone would create a major economic and political problem. In such a situation, the probability that exports could fully compensate for the internal consumption contraction is very remote.

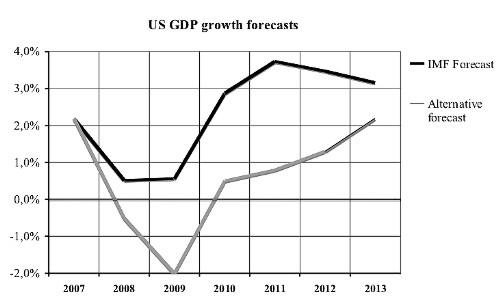

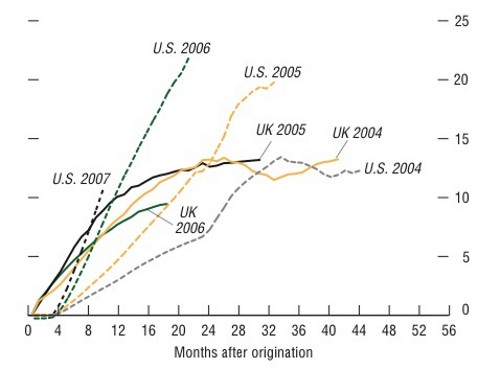

Third, US public finances are to be heavily constrained in forthcoming months, making a strong contra-cyclical budget policy unrealistic. The housing market crisis and the fall of house prices have already strained local budget revenues in 22 states and in the District of Columbia. The total amount has been estimated to 39-41 US Dollar billions for Fiscal Year 2009. In five other states (Delaware, Louisiana, Michigan, Mississippi and Tennessee) significant budget shortfalls are to appear in FY-2009, but the size of those deficits is still not available[59]. As local budgets cannot run a deficit the Federal budget is to cover those deficits, for a probable amount of 40 to 44 USD billions or local expenditures are to be dramatically curtailed, a process adding its weight to already existing depressive factors. In the same time the US bank and insurance systems are to be cleared of accumulated bad assets. So far the Fed agreed to take USD 29 billion of assets onto its balance sheet. However the extent of the bad assets issue is much larger and clearly beyond Fed means. A special defeasance system is to be created to rebuild confidence and it could entail buying for USD 450 to 600 billion of “bad” assets[60]. This would have to be done probably by the end of summer 2008, and the full budget burden (or between 15.0% to 20.0% of the current Federal Budget) is to be carried during FY-2009. If we introduce into the picture growing costs of the War in Iraq and in Afghanistan, it becomes obvious that we can’t expect the kind of strong contra-cyclical budget policy the US policy currently needs to avoid being trapped into major a recession. By any extent the FY-2009 budget deficit is to be quite large and so is to be the FY-2010 one, and this without a strong pro-active policy. As already mentioned, no relief can be expected from local budgets, which by the way have still not recovered from the beating they took in 2001 and 2002. In this context economic forecasts have to be bleak. If we take into account all depressive factors, including their impact on behaviours through the creation of a highly unstable context, even the IMF forecast, usually described as particularly bleak, could be seen as unduly optimistic. The US economy is to experience the worst of the crisis by late 2008 and early 2009, with some improvements by late 2009 and a slow recovery beginning by spring 2010 (Figure 4). It is to be understood that the alternative forecast is not a “worst-case scenario” and does not introduce the possibility (quite real) of a sudden deterioration of the bank crisis or a run against the US dollar.

It is then reasonable to expect that the US economy is to run through a serious recession, whose effects are to felt till 2011 at best. Unemployment is to increase strongly in 2009 and 2010 and there will be no improvement before probably 2012, when the GDP will recover its actual 2007 level. The recession duration is to be much longer than what the US economy has suffered since 1950. The “Subprime” crisis is then not to be a short-duration “blip” in the US growth, not just because of the banking crisis severity but because this crisis exposed to what extent the growth experiences between 2002-2007 has been unsustainable and to what extent economic and social policies implemented in the wake of the early 80’s “Conservative Revolution” have weakened the US economy growth engine. The possibility that the US economy will after 2011/2012 enter into quite a long slow-growth period (1.5% to 2.0% a year) can’t be ignored, but for the implementation of an economic policy addressing structural factors of the current crisis. I. Impact on economies of EU countriesForecasting the economic climate among EU countries implies first to discriminate between Western and Eastern Europe, then to discriminate between countries where “Conservative Revolution” principles have been more thoroughly implemented and others where the traditional post-war European socio-economic model is still partly functional. III.1. Western European heterogeneity. Main Western European countries are not making for an homogeneous economic group. This is true not just because Great Britain is not part of the Euro Zone but also because a strong heterogeneity inside the Euro Zone. The common currency has so far failed to induce a structural convergence process. One important difference is coming from the fact that some economies have followed the US “Conservative Revolution” pattern more closely than others. This can be seen when comparing general savings (table 3). Great Britain looks closer to the USA than Germany, France and Italy. Actually, Spain is certainly closer to Great Britain than to France in this respect.

In economies where the US pattern is more predominant we find a high household indebtedness ratio (124% of GDP in Spain, 130% in Great Britain and Ireland), a large involvement of the banking sector in credits to the real-estate sector (up to 65% of bank assets in Spain) and consequently a high vulnerability to a mortgage crash similar to the US one. This situation is in GB the direct result of growing poverty and inequality[61]. If the British economy has grown relatively fast since the mid-90’s the very unequal income distribution has sown the seed of a credit-dependence undermining directly the growth model. To a large extent the British economy looks as exposed as the US one. The NorthernRock bank failure of Fall 2007 is here clear a symptom. So far the British government reacted strongly. NorthernRock was nationalized to prevent a general bank run. Still, more difficulties are looming ahead. In the latest edition of the World Economic Outlook the IMF is forecasting a slow down of the growth rate from a 2.75% average for 2000-2007 to 1.6% for 2008 and 2009. This is probably overly optimistic. The high uncertainty pervading the financial system combined to losses households suffered in pension funds during the last winter is to probably push up the saving rate with a contraction of personal consumption spending. The fall in home prices is to have the same downward wealth effect than in the US economy. The yearly rate of growth could be in the 0.5%-1.0% range for 2009 and recovery is to happen later than forecasted by the IMF (possibly 2012/2013).

The situation in Spain is not without similarities with Great Britain and the US economy. The strong growth the Spanish economy experienced till 2000 was largely pulled by a highly speculative real-estate market. Fuelled both by internal and external demand (mostly in tourism resort areas) new house constructions on a 12 months basis reached 800,000 in 2006. However, as Spain was in the Euro Zone an economy were “Conservative Revolution” principles have been more significantly implemented than in Germany, France or Italy, this high demand was not pulled by a commensurate increase in income but by a growing indebtedness. Household debt reached 124% of National Income by September 2007 (against 67% by end 2000). As a result Spanish household solvency has significantly deteriorated. The average yearly mortgage payment rose from 31.3% of household average disposable income in 2003 to 45.4% in September 2007. Spanish banks were also extremely active in the real estate sector and 65% of their assets were related to this sector by 2007. Securitization of mortgage loans has been at the forefront of credit expansion since 2002. During 2000-2007, this expansion was made possible by steady rise in house prices. In 2007 the squared meter average price in urban areas was higher by 20% in Spain than in France, where income standards are still higher[62]. To a large extent, Spain looks like the European version of the US “false growth” situation described here above. The real estate sector began its downturn during fall and winter 2007. The number of new constructions on a 12 months basis dropped sharply to 375,000 early 2008. Some forecasts are putting this figure to 100,000 by the end of 2008, which would imply to any extent no new constructions during Summer and Fall 2008. Household solvency is to be tested during 2008. So far delinquencies have been very few, with a record low 0.87% in 2007. However with the sharp increase of credit repayment burden, solvency heavily depends from household income growth in coming months. With Italy, Spain is the Euro-Zone country where unit labour costs have increased the fastest since 2000[63]. This, combined to the Euro change rate overvaluation is to hit hard competitiveness. Combined to a huge inflow of immigrants, this is to push down wages in the next two years. If the process happens through high inflation (nominal wages still increasing but slower than prices) the shock on household solvency is to be limited and the rate of delinquencies is not to increase too fast. However, as Spain can’t devaluate its currency, an inflation rate higher than the Euro-Zone average is to increase the trade deficit (already expanding fast) and would ultimately make a correction on wages necessary. If the process happens without an inflation burst, that is if wages nominal growth is to stagnate during the next two years, then the effect on household solvency is to be important. The rate of delinquencies could quickly jump to 2% and over. This would be serious a problem for Spanish banks. One can assume they are to restrict lending from Spring 2008 on to reduce their exposure to the real-estate credit risk. This move is to have a strong impact on economic activity. In such a situation, and considering both the low level of household personal savings and the high debt burden on Spanish households’ shoulders[64], a consumption crunch is unavoidable. It is to be compounded with a strong reduction in investments, directly linked to the current contraction of the house-building sector. However, this could not be the end of the story. If a serious growth slow-down is to happen in Spain, it could degenerate into a much worse crisis. Spanish banks are highly vulnerable to a strong real estate sector downturn. Spanish banks are also vulnerable to an external shock. They are exposed to a considerable extent to an economic downturn in Mexico. If, as forecasted here, economic activity is quite depressed in the USA by Fall 2008, the impact on Mexico is to be significant. In the same time, Mexico is a country directly threatened by Chinese competition. Mexican production, which had a significant quality advantage compared to Chinese exports in 1990 regressed when China closed the gap. Mexico is then the example of some Latin-American countries, which are threatened to be caught between the US recession hammer and the Chinese anvil[65]. A strong recession in Latin America could then have a serious disruptive effect on Spanish banks, at a time they are to be weakened by the real-estate market downturn in Spain. Even if their profit ratios are still good by spring 2008, they are to suffer a serious shock by next fall. A bank shock in Spain would have tremendous consequences not just inside the country, but also in the whole Euro-Zone. The Spanish government has already announced an economy rescue plan and is to inject 8 Euro billions by 2008 and 10 by 2009. This is a step in the good direction, but is still much too conservative. As the government debt has been very small in Spain (34% of GDP) and considering the fact regional governments have more leeway for actions than in the US system, one can assume that public authorities are to act in a way to prevent the crisis to drift out of control. However, there is to be no room for error in economic policy. In such a situation, the yearly GDP growth is to be more depressed than what is currently expected. Yearly GDP growth averaged 3.6% in Spain for 2000-2007. The IMF is now forecasting 1.8% for 2008 and 1.7% in 2009. This again is probably optimistic. Growth could fall under 1.5% in 2008 and under 1% in 2009 even without assuming a major bank crash, which could plunge the Spanish economy into a fully-fledged depression. The situation of Germany is of particular interest as the economy has been for long the leading one in Western Europe and is exerting a powerful influence on its neighbours. To some extent too, Germany, like France or Italy is still closer to the traditional Western European economic and social model than Great Britain and Spain.

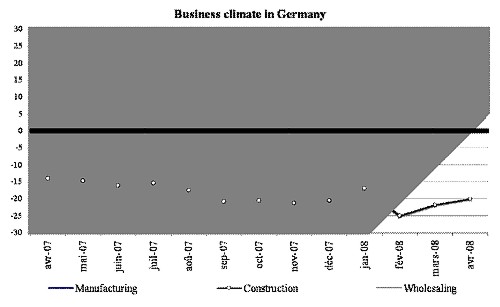

Despite reforms implemented by the Shroeder’s government in 2004 and 2005, which have boosted economic activity, the business climate has been steadily deteriorating since spring 2007. It has been argued that the German industrial structure could shield the economy from the impact of a strong Euro. However, since summer 2007, when the Euro began to appreciate quickly against the US Dollar, business expectations have fallen to a significant extent. There is currently a strong gap between the assessment of the economic situation (which is still positive) and business expectations. This is particularly true in manufacturing industry. Here the number of survey responses rating the situation as “good” overtakes responses rating the situation as “poor” by 30 points. However, when it comes to expectations, the number of responses rating the future situation as “most unfavourable” overtakes ones rating the future situation as favourable by 9 points. This huge discrepancy between situation assessment and expectations is the result of the sharp drop in future contracts. The current situation is assessed on the basis of contracts made 6 to 12 months earlier. For the April 2008 IFO survey the situation assessment reflects the German industry order book as it was late spring 2007. However, the strong Euro is making German products non competitive on various markets. The German industry order book is deteriorating fast, which explains why expectations are gloomy. The very fact that now event the German Minister of the Economy is protesting against the Euro exchange rate is a clear signal the situation is deteriorating fast in Germany[66]. As German banks have been quite exposed to the “Subprime” crisis, and with some pension funds already experiencing difficulties, the personal saving rate of an aging population is to increase in forthcomings months. Investments have considerably slowed down in 2002 and 2003 and never completely recovered. Internal demand is then not to be a substitute to dwindling exports. One can then expect economic activity to slow down significantly from the end of spring 2008 and on. The extent of this process is still difficult to forecast. IMF figures are particularly bleak for Germany, with a GDP growth of 1.4% in 2008 and 1.0 in 2009 and the German government ha modified its own forecast and is now converging toward equally bleak predictions[67]. However, IMF forecasts for Germany are not taking into account either a US recession deeper than forecasted, nor potential side effects of a Spanish crisis on German banks and insurance companies. Here again, IMF forecasts are to be understood as “best-case” predictions. The French economy has been widely described in the internal political debate as “stagnating”, which has been a highly unfair judgement. Actually the French average yearly growth for 2000-2007 has been significantly higher than in Germany or Italy, and comparable to Netherlands. The French saving rate is higher than in Great Britain and Spain and if the government debt is higher than in Spain (66% of GDP) household indebtedness is significantly lower than in Great Britain and Spain. French banks seems to have been less exposed to the “Subprime” crisis than German or British ones and the French real estate market has been much less affected by speculation than ones of Great Britain and Spain. Mortgage backed loans are not very used in France and this has reduced the potential for a bubble during the last three years. It is however true that the French industry vulnerability threshold to the Euro exchange rate is somewhat lower than the German industry one. The strong Euro is a serious problem when the EURO/USD change rate reaches 1.25 USD for 1 Euro, when it seems to be a serious problem in Germany at 1.40 USD or higher. Another disturbing point is the current government economic policy. Since general elections of June 2007, the new government is implementing a string of structural reforms aiming at increasing the labour-market flexibility and diminishing labour costs. Unfortunately these reforms are to make their impact felt during 2008 and 2009 when the demand is to be already depressed by the crisis in neighbouring economies. Tax breaks included in the French “fiscal package” are much too concentrated on the income upper strata to have an effective impact on consumption. To some extent the policy the new Prime Minister Mr. Fillon is currently advocating is not without similarity by the one Pierre Laval implemented in 1935. Such a policy is ill-timed and will probably increase the French economy vulnerability during 2008 and 2009. So far, the French government has not showed a willingness similar to the German one to publicly acknowledge how bad the situation is to be. As noted in the foreword, the fact that growth for 2007 has been a bit better than expected is fuelling a completely unwarranted optimism about the current economic policy effect. Results for March 2008 are gloomier. The manufacturing industrial sector production fell by 1.5%, and equipment goods went down by 1.1%[68]. A 1.7% yearly GDP growth target has been so far maintained. The actual growth nevertheless is more probably to be under 1.5%. Italy has known a very sluggish growth during the last 5 years. By any extent Italy is the economy suffering the most of the Euro over-valuation. So far Italian banks have not disclosed significant losses and write-offs but the Italian banking system is not extremely transparent. Italian insurance companies have suffered from the global financial crisis and it would be surprising if Italian banks were to fully escape the financial blood bath. Consumption is already quite depressed even if investment is like in France still at a higher level than in Germany and Great Britain. With a huge public debt (over GDP 100%) the new conservative Italian government is to lack room to manoeuvre.

Alternative estimates: result of author’s pooling of forecasts made in 3 French, 1 Swiss, 2 German and 1 Belgium bank, late April 2008. To sum up, Western European countries are to suffer significantly from the current crisis even if individual countries are to experience very different situations. The crisis is to be particularly hard in the two countries where economic reforms inspired by the US “Conservative Revolution” had been the most important, Great Britain and Spain. Even without the ‘worst-case’ scenario of a massive bank collapse in Spain, other countries are to know a serious recession at the very least till 2010 (table 4). There is then no doubt the Euro Zone is to face significant economic hardship in years to come even if the recession is to be less severe than in the US economy. III.2. Impact of the crisis on Eastern EU economies. Eastern European countries have known a strong growth from 2000. But for Bulgaria they have all overtaken effect of the 1990’s depression. This high growth has been generated by a strong investment process, which has been helped by an important FDI flow, concentrated on Poland, Hungary and the Czech Republic, and also quite pro-active public policies. However these last have generated a strong budget unbalance, particularly in Hungary, Poland and the Czech Republic, as well as a strong current account deficit[69]. Labour productivity increased, but from a very low initial level[70]. An important point to be remembered here is that the OECD export similarity index increased faster in China and India than in most Eastern European countries from late 70’s to today. By 1983, Hungary and Poland were at the same level than China (8%) with India slightly lower (7%) and Rumania probably trailing even lower. By 2005, Poland has reached 17%, Hungary 13% and Romania 8%. However, China has reached 21% and India 16%[71]. Eastern European economies developing along the path of low-cost industrial goods exporters are to suffer an ever greater competition from East-Asian economies if they are not able to make considerable gains both in productivity and production quality in forthcomings years. To some extent the Eastern European economies development path was under fire even before the beginning of the current crisis.

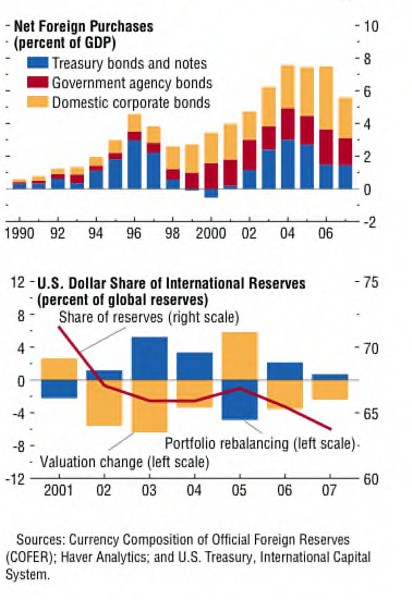

There are no doubts however those Eastern European economies are to be hit hard by the current crisis in forthcomings months. Factors pointing to this direction are numerous. (i) If economic activity is to slow down in the Euro zone and particularly in Germany and France demand is to be seriously constrained. Not only is activity to slow down but the trade deficit is to widen if Eastern European exports toward the Euro zone are to be reduced. (ii) Banks in Eastern European countries are heavily dependent from Western banks, be they European or US. The current credit crunch is then to hit hard the Eastern European banking sector. (iii) The combination of export reduction and reduced activity is to reduce budget revenues growth during 2008 and 2009. As most Eastern European countries are running high budget deficit and considering the fact local financial markets are to be short of liquidity for a time, an adjustment process on the expenditure side is unavoidable and is to contribute too to economic growth reduction. (iv) Most eastern European economies have extremely unfavourable energy balances. The rise in oil prices is to have a strong impact both on economic activity and inflation. This would also contribute to further deficit of the trade balance. Economic growth is then to slow down to a significant extent during 2008 and even more in 2009. This growth recession is to be combined with increased trade deficits and rising inflation. The very positive economic image Eastern European economies benefited from during last years could be quickly overturned, would a significant bank crash or some political troubles happen during coming months. By any extent, the FDI flow is to be reduced, raising a serious current account problem. The combination of the crisis short-term impact and more long-term issues could have significant changes on the Eastern Europe economic climate. III.3. European economies through times of crisis: diverse and not unified? The current crisis effects on European economies are to be widely different from one countries group to another. There is nevertheless no doubt that Europe is to be hit hard and that the Euro zone is to know a significant and long recession. Countries whose economy has come closer to the US model are to suffer most. Great Britain, Spain and Ireland are here noteworthy. Spain is certainly the most vulnerable economy, but Spanish public finances are also ones allowing the greatest freedom of action. The strength and timing of public authorities response to the crisis are here a crucial factor. The three main Euro zone economies, Germany, France and Italy are also to suffer from the crisis, but are less exposed than Great Britain, Spain and Ireland. The economic downturn is to be more spectacular in Germany than in France as the gap between economic actors perceptions of the present and the future situation is the greater in Germany. Economic policies are the main issue in France and Italy. In France, bad timing and a government unwarranted fascination with “Conservative Revolution” economic model could harm economic activity more than expected. The Euro Zone displays a relatively stable business cycle intra-correlation at a low to moderate level[72]. Growth trends among Euro-Zone countries appear to be weakly correlated. On the other hand, output-gaps are better correlated. However, this output-gap correlation can be identified much before the EMU, actually till mid-60’s[73]. Part of the relatively good business-cycle convergence one can find in the Euro-Zone comes from the fact that the Big Four economies (France, Germany, Italy and Spain) were actually relatively well synchronized in the 70’s and the 80’s. The EMU has increased convergence for smaller countries part of the Euro-Zone but has not significantly modified the pre-EMU situation of the “Big Four”. The very fact that the output-gap volatility among Euro-Zone countries is diminishing could be as well a proof of a convergence process than the result of the general growth slow-down the Euro-Zone experienced the last six years[74]. Actually, a relatively recent study on economic divergence under external shock has shown that the Euro area would be more prone to divergences than other currency areas[75]. This is the result of diverging path of inflation persistence among Euro-Zone economies, a problem apparently rooted in structural differences[76]. From this point of view intra-Euro area divergence seems to be much more severe than one the output-gap correlation analysis suggests. The point is significant as one impact of the current crisis could be a combination of depressed demand and strong inflationary pressures through high natural-resource prices. If so, the impact of the crisis on the Euro-Zone could increase macroeconomic divergence. Eastern European economies, which but for Slovakia are not Euro-Zone members, display too a strong heterogeneity. Some countries are already quite well correlated to the Euro-Zone, like the Czech Republic and Poland. Some countries are weakly correlated in a stable way (Slovakia and Romania). Some countries are showing a trend of de-correlation with the Euro-Zone (Hungary, Bulgaria)[77]. This situation implies that economic consequences of the current crisis could exacerbate differences among EU economies. We found that but for Spain, where we have some specific problems, the other three economies of the “Euro Big Four” would react in a quite similar way. This is consistent with econometric data on the “Big Four” correlation. However, outside the “Big Four”, the picture is much more diverse. Economies from the Eastern part of the EU are not just different from the EU core, but they are also quite diverse in their own dynamics. A strong economic slow down in the Euro Zone would strike more Poland and the Czech Republic (where industrial integration with Germany is pretty high), than Hungary, Slovakia, Bulgaria and Romania. Eastern European economies could experience a brutal downturn aggravated by a strong framing effect by the end of 2008 and early 2009. The buoyant growth experienced in those economies was already quite frail before the crisis outbreak. One central issue could be substituting new markets to the depressed Euro zone. Russia and the CIS could here be a partial solution, but this would imply some climatic restatements of national policies. Hungary, Romania, Bulgaria and Slovakia are here probably in a better situation than Poland and the Czech Republic where industrial activity is strongly dependent to the economic climate in Germany. To some extent, the same reasoning applies to some Nordic economies. The Finnish and Swedish economies are already pulled by the strong Russian growth (and Norway is obviously a special case). Being relatively small economies, both countries could run through the current crisis with much less problems than other European economies. One important point usually not stressed when discussing the possible impact of the crisis in Europe is the existing asymmetry between Germany on one hand and France and Italy on the other to Euro overvaluation consequences. This asymmetry is raising a difficult problem for shaping a unified policy. If the USD to Euro change rate is to stay over 1.55 USD for 1 Euro, the German economy is to suffer enough to make this asymmetry irrelevant. It would then be possible to devise a joint policy. However, if the exchange rate would be comprised between 1.45 and 1.55 USD for 1 Euro, consequences would be so asymmetrical that devising a joint policy could be impossible. This is to be correlated with Angeloni and Ehrmann study of inflation differentials in the Euro Area. If a demand shock and a cost-push shock are already to significantly increase the divergence process in the Euro area[78], this asymmetry could well become unmanageable. The Euro zone could then be strained beyond the rupture point. I. ConclusionThe current economic crisis is definitely a major economic event, which is to be compared in scale and scope only with the 1929 one. This crisis is to change to a considerable extent the global economy as we know it. Not only are we to experience an important economic power shift, but the crisis is to speed up some major paradigm changes. The crisis is to have an impact well over just the financial sphere and it is to unfold with all its consequences during Year 2008 second part and early 2009. IV.1. A crisis of Neo-liberal economics. The US but also European economies are to enter a recession, which is to be both deeper than what is usually though and more protracted. In the US economy, this recession is probably to be the more severe experienced since 1950 as it corresponds to a structural crisis of the growth path experienced since the 90’s. Beyond the mortgage-market crash and the credit crisis, there is the collapse of the economic and social model grounded on a highly unequal income distribution fostered by the combination of tax policies and the impact of the free-trade regime on worker wages. What “Conservative Revolution” has ultimately created was a highly dysfunctional social and economic system, a French economist aptly called “Dissociété”[79]. It would then be a mistake to reduce the scope of corrective actions just to a better regulation of finance and particularly of structured finance. Such a regulation is needed beyond doubt and one has to welcome various proposals going in this direction[80]. However, exposure to financial markets is to be reduced too as technical regulations are no more than a stop-gap. The disruptive effect of the unbound Prometheus Finance has been in the last two decades begins to be better appreciated[81]. To go farther, this is the whole neo-liberal model, with its unequal tax-breaks, reduction of public spending and non controlled opening-up, which is to be questioned. The current crisis is not the “Subprime crisis”. Subprime mortgage loans have been nothing but a symptom of much deeper social and economic disorders neo-liberal economic policies have created and we can read through the explosion of inequality, the collapse of savings and the huge household indebtedness. European economies are to be strongly affected too, but to a lesser extent than in the USA. The main reason is that usually, but for some countries like GB or Spain, the “Conservative Revolution” has less affected the national institutional framework than in the USA. The situation is to be more closely comparable to what we have known in the 80’s and 90’s. Nevertheless, in countries where the social and economic structure has been reformed deeper along the line of Neo-liberal economics, the threat of a major depression is clearly looming. It would then affect neighbouring countries. There is then no reason to think that a country could be spared from the crisis but for implementation of radical and voluntarist policies aiming at dismantling what “Conservative Revolutions” have created in the last two decades. However, this recession is to have several specific characteristics compared with previous similar episodes in the 80’s and 90’s. First, the recession is to be mainly one of “Western” economies. The uncoupling process frequently alluded about since last winter appears to be substantiated. The crisis impact on East Asian economies is to be pretty mild. A similar situation is to happen with Russia. One can then reasonably predict that world growth is to be pulled by China, India and Russia at least till 2010 and possibly later. The impact of the Russian fast and robust growth is to be felt even inside the EU. This situation is to change economic relations on the European continent to a significant extent. Second, this crisis combines short-term dynamics and long-term ones. It is basically a crisis of the economic model “Conservative Revolutions” have fostered since 1980. It is also a crisis of the economic world order called “Globalization”. This combination of short and long-term dynamics makes an early and fast recovery not a very probable event. Even if the worst of the crisis is to be felt by winter 2008-09 in the US economy, and probably during spring or summer 2009 in Western European economies, the recovery is to be protracted and plagued with high instability at least till long-term crisis factors will not be addressed. We are entering a new economic context, which is to frame economic behaviours and thinking for quite a long time. The current crisis is also to probably combine its effect with the collapse of the WTO “Doha Round”[82]. IV.2. Back to international money and finance. In the monetary-financial sphere, two issues are to come to the forefront and are to have a deep impact on possible recovery paths. The first one is obviously how deep the US Dollar could fall in coming months, and how long could it stay at a low level. There is so far a limited consensus among analysts to expect the Euro to USD exchange rate to stabilise by 1.48 USD to 1 Euro by end 2008. This could be but one is to be aware of factors weighting down on the USD exchange rate. The US public deficit is to grow to a considerable extent for FY-2009 and possibly FY-2010. As it would be counter-productive to raise interest rates to make US T-Bonds more attractive, part of the US newly issued debt is to be monetized. By the way the stronger the recession the less attractive would be investment in the US economy. Those factors are to seriously reduce incentive to buy USD denominated debt (be it in T-Bonds or Agencies Bonds). If current holders of US debt instruments are to switch even for a limited share of their portfolio toward other currencies (and particularly the Euro), the USD exchange rate is to fall deeper than currently expected. Already, there is a declining trend in foreign purchases of Treasury and Government Agency bonds. Combined with US Corporate bonds, net foreign purchases reached nearly US GDP 8% in 2004. In 2007 we were already at 5.7% (Figure 7). It would be safe to assume that foreign net purchases are to be much lower in 2008 and 2009. The US Dollar represented more than 72% of International reserves in 2001. This share has already dropped under 65% in 2007 and is to still go further down in forthcoming years.

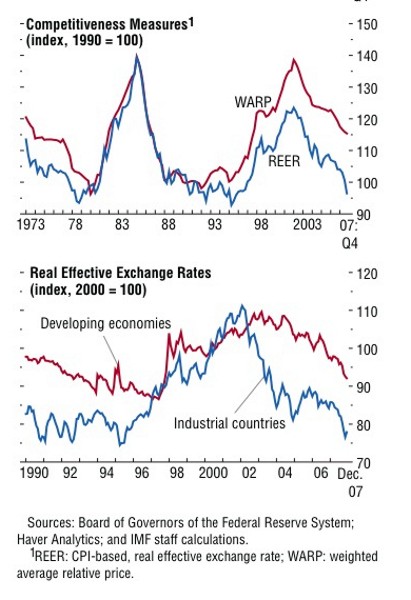

Another “surprise” in Shackle’s sense on this point could well trigger a run against the USD. This could have tremendous consequences, igniting an even greater speculation on commodities than currently and creating such havoc in the US economy that estimates presented in this paper could well appear as over-optimistic. An important point to be kept in mind is that if the US Dollar has considerably fallen by comparison to the Euro, it has so far still not reached its lowest level as experienced in 1978/9 or 1990-1994 (when compared to industrial countries). Both the competitiveness index and the Real Effective Exchange Rate index are showing there is still some room for further devaluation (Figure 8). This is an important point to be kept in mind, as structural factors pushing the US Dollar down are actually even greater than in the late 70’s or the early 90’s.